আরও দেখুন

11.12.2024 12:37 AM

11.12.2024 12:37 AMThe UK's industrial sector has responded to the new budget presented by the Labour Party with decreased business confidence and slower hiring. While considered secondary indicators with limited direct impact on the pound's exchange rate, several metrics clearly show a slowdown: business confidence in November fell to its lowest level since January 2023, and the BDO optimism index dropped by 5.81 points over the month to 93.49, marking the steepest monthly decline since August 2021. According to BDO, the decline observed in both the services and manufacturing sectors "likely reflects an immediate reaction by businesses to statements made in the autumn budget."

Job vacancies in November fell at the fastest pace since the onset of the COVID-19 pandemic, with demand for personnel decreasing "sharply and at an accelerated pace."

On Thursday, the NIESR will release its estimate of GDP growth for November. Friday will be critical for the pound, with the release of data on the trade balance, industrial production, and GDP for October. While these data points may not significantly impact the pound's exchange rate on their own, they are important for forecasting the outcomes of next week's Bank of England (BoE) meeting. Before the BoE meeting, several crucial releases are expected, including preliminary PMI data for December and reports on the labor market and consumer inflation. These reports will serve as the basis for the market's final projections.

The BoE's decision remains unclear. The market assumes the rate will stay at 4.75%, but policymakers' comments are contradictory. MPC member Catherine Mann argues that inflation in the services sector remains "stubbornly high," driven by wage growth, and has stated she will vote against a rate cut. At the same time, MPC member Swati Dhingra, on the other hand, highlights that monetary policy is restrictive, suppressing supply volumes, investment, and consumption, suggesting that policy easing is needed.

Given these conflicting perspectives, the pound lacks clear drivers for continued growth and has limited reasons for further decline. The bearish trend remains intact, but whether the corrective phase has ended is unclear.

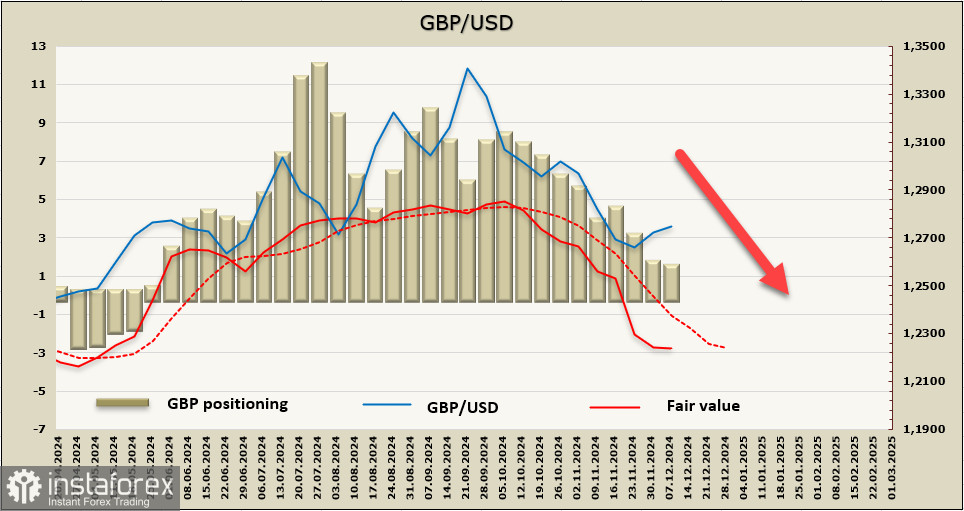

The net long position in GBP has decreased by £169 million to £1.53 billion. Despite this relatively small reduction, the position has moved closer to neutral. The estimated price has fallen significantly below the long-term average, but the decline has slowed over the past week.

GBP/USD is currently in a phase of corrective growth, which is likely not yet complete. The pair has yet to reach the 1.2830/40 resistance zone, identified as a potential turning point for a southward reversal. While another attempt at growth cannot be ruled out, it is unlikely to be substantial. A more probable scenario is a resumption of the downtrend toward 1.23, the long-term target.

You have already liked this post today

*এখানে পোস্ট করা মার্কেট বিশ্লেষণ আপনার সচেতনতা বৃদ্ধির জন্য প্রদান করা হয়, ট্রেড করার নির্দেশনা প্রদানের জন্য প্রদান করা হয় না।